Carvana (CVNA) Challenges

Summarizing the 2026 CVNA short reports

Disclaimer: This post is not financial advice, and is not a solicitation to purchase or sell any securities. For more info, please review the disclaimer.

In 2026 Carvana has been the subject of short reports from both Gotham City Research and Abelian Analysis.

Gotham City Research’s report is imposing, running to more than 70 pages as well as supplementary filings and annual reports for two related parties. I will summarize the recent short reports as well as the company’s response and Gotham City’s follow-up.

Why me?

I have followed CVNA for years and lost money shorting their 2023 resurgence. I also bought a car from Carvana and, while I wasn’t blown away, I understand how it could be the future of used car buying.

Gotham Report

Gotham City’s short report primarily boils down to the following key claims:

DriveTime is owned by Eric Garcia II, the father of Carvana founder Eric Garcia III. DriveTime is inflating Carvana’s profits by over a billion dollars between 2023 and 2024 in an attempt to benefit from the higher multiple given to Carvana versus the privately held DriveTime.

Evidence of DriveTime attempting to inflate Carvana’s profits includes $1B in net debt issuance for DriveTime over the 2022-2024 time period.

DriveTime had negative adjusted EBITDA (after portfolio debt expense) in 2023 and 2024 compared to high single-digit adjusted EBITDA from 2009 to 2013.

DriveTime has scaled significantly in the past decade with revenue growing 3.5x and 65% greater revenue per employee, yet operating margins are worse now than they were in 2010-2013. Gotham claims this is evidence of artificially low margin due to DriveTime subsidizing Carvana.

Gotham City also claims that Bridgecrest, another related party owned by Eric Garcia II, is inflating the gain on loan sales for the company.

Gotham City also claims that Carvana’s 10-K will be delayed and the 2023 and 2024 10-Ks restated, along with Grant Thornton, their current auditor, resigning.

One counterpoint: Gotham claims Eric Garcia II extracted roughly $300 million from DriveTime, yet also suggests he’s trying to maximize family wealth by boosting Carvana’s reported economics. Since Carvana trades at a much higher multiple it would make sense for Garcia to subsidize Carvana’s earnings with the $300M instead of withdrawing it in cash for himself. The market, in turn, would have given Carvana an even higher multiple, and the Garcia’s would have profited even more as they’ve sold billions of dollars of stock in the last two years.

Gotham Report Analysis

Now let me provide my analysis of the following three points:

There is clearly evidence of related party transactions as Carvana discloses in their 10-K. Other short sellers like Hindenburg have also pointed to these transactions, which may be inflating profits or decreasing warranty costs as well as other financing and servicing costs. These arrangements are suspicious enough to me that although I don’t see a smoking gun, I would likely avoid investing in Carvana or significantly decrease my estimates of their run-rate profitability to take into account potentially temporary favorable terms here.

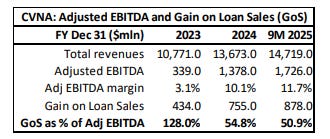

Gotham City also claims inflated gain on loan sales. This argument is much less compelling to me, as we can see the gain on loan sales decreasing as a percentage of adjusted EBITDA. Furthermore, it obviously makes sense that Carvana may be originating loans that are immediately profitable to Carvana. Dealer financing is a core profit driver for used car dealers. After dealers make a loan, they are then able to sell these loans and immediately recognize a profit on the loans they’ve made to customers wanting to buy their cars. The rest of this claim reduces back to suspicious related-party transactions per #1 above.

Gotham City claimed Carvana’s 10-K would be delayed and Grant Thornton would resign. This has clearly proven false as Carvana filed their 10-K on time. It’s too soon to see if the 2023 and 2024 10-Ks will be restated because that could happen at any point in the future, but so far it has not occurred. I would judge this claim to be extremely optimistic, overly promotional, and ultimately false.

Abelian Report

An Abelian Analysis short report boils down to a claim that credit quality is deteriorating for Carvana asset-backed loans as they have started to offer a small subset of loans to very suspect car buyers with poor credit ratings. Abelian’s main claim is a forecasted increase in defaults due to poor consumer credit and car repossessions leading to a significant increase in Carvana’s cost to package and sell future asset-backed securities hampering their ability to sell cars.

Abelian Report Analysis

Much of Abelian Analysis’s post is about the future, and I don’t have a crystal ball. To some extent, we’ll have to wait and see if this year the ABS is underperforming, leading to more expensive financing for these asset-backed securities. However, I’ve heard many pitches and claims like this in the past, and often times credit quality is much stickier and better than people forecast. If there are signs of significant losses, Carvana is likely to be able to raise the rates they charge lower-quality consumers and, in turn, pass those higher rates on to investors. So, it is hard for me to imagine this as an existential threat to Carvana’s business model.

Conclusion

Overall, there are persistent suspicions around the related-party transactions between DriveTime and Carvana. However, Gotham City’s report lacks a smoking gun, and the poor operating results they point to can also be explained by weak auto loan performance in 2022-2024. Abelian’s report is more forward-looking and claims future auto loan performance will be bad. However, I don’t believe this is an existential risk to Carvana’s business model as they can adjust pricing and shouldn’t be disadvantaged compared to other auto dealers.

I have no position in Carvana and remain skeptical of some of the related party transactions. I don’t see Carvana having a significant moat here, but perhaps I underestimate the logistical difficulty of the automotive network they have compared to eBay autos, CarMax, or Amazon getting into the space. At current prices, CVNA is too expensive for me, and I will remain on the sidelines.

Resources:

Thread responding to Gotham Short Report

JPM executive summary response to Gotham Short Report

Twitter thread - Abelian data correction

Thank you for the detailed article, well done. I’d like to point out Carvana’s defenders keep missing the core business issue: the securitization model already proved its fragility the moment Ally Bank pulled funding, one stress event (the very first event) and the entire securitization engine seized instantly. CVNA was out of liquidity immediately & quickly sold $800m to an unknown party that started a series of events. It triggered a short seller report from Hindenburg, triggered an SEC investigation and a federal securities fraud lawsuit (nearing deposition phase). This isn’t about forecasting the future; the failure is already happening. No finance company can survive long‑term while approving every application, verifying no income, stuffing 33%+ of loans with negative equity, and stretching used‑car borrowers to 72–84 months. Carvana is putting borrowers in loans they cannot afford. There is no interest rate high enough to outrun that credit mix once securitization tightens, and history is absolute on this point: not one used‑car retailer dependent on securitization has survived more than a couple credit cycles. The idea that Carvana can simply “raise rates” ignores the structural truth that securitization cannot survive a real downturn, and that downturn is already underway.